Simple Interest on Loans: Formula, Examples, and Comparison with Monthly Payments

Simple interest is one of the cleanest finance formulas because the interest grows linearly from the original principal. That makes it ideal for early finance lessons and rough comparisons. The same simplicity is also its limit: many real loans do not behave this way, especially when they use monthly payments and amortization.

This is why simple interest is useful educationally even when it is not the full story in practice. It gives you a clean way to see how principal, rate, and time interact. Once that relationship feels natural, more complex payment models stop looking like magic and start looking like extensions of a core idea.

Applicable Use Cases

Simple interest is useful in school finance chapters, quick borrowing estimates, short-term note problems, and sanity-checking rate claims. It can also help readers understand the relationship between principal, rate, and time before they move into more complex loan schedules.

If someone is comparing several borrowing offers, simple interest can provide a baseline intuition. It will not replace actual lender documents, but it can help a reader see whether a claimed number feels plausible or wildly off.

That baseline matters because many people confuse any interest calculation with any loan calculation. In reality, different borrowing products use different balance rules. Simple interest gives you the straight-line version first.

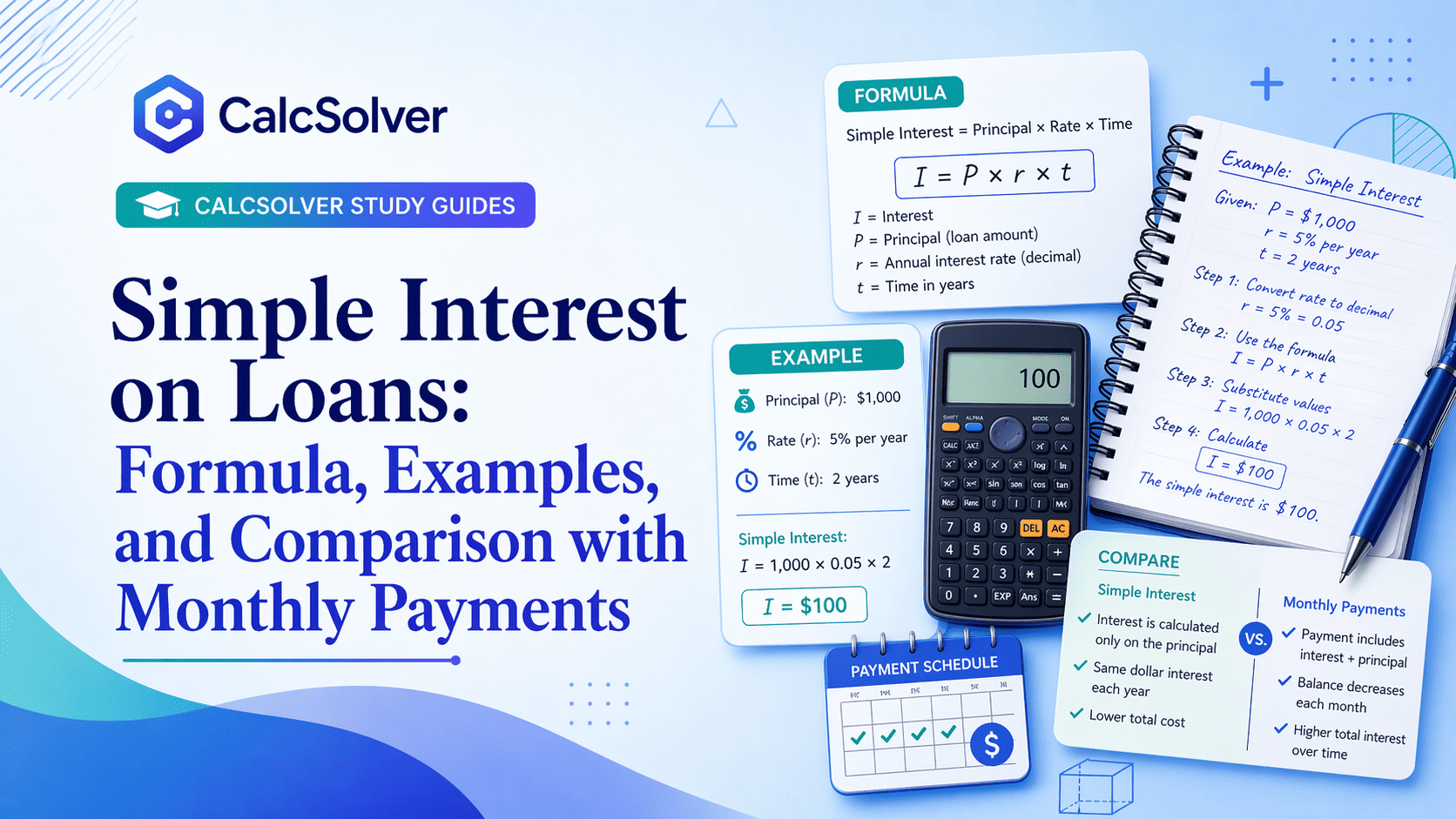

Formula Principle

The core formula is I = P * r * t, where P is principal, r is the interest rate in decimal form, and t is time. Total repayment in a simple-interest classroom setup is P + I.

The important idea is that interest is based on the original principal, not on a growing balance. That is why the graph is linear rather than compounding upward. As soon as a problem starts using monthly payments on a shrinking balance, you are moving away from pure simple interest and toward amortization.

That distinction is where many readers get lost. A simple-interest problem tells you to look at one base principal and let time scale the interest. An amortized loan recalculates around the payment schedule and remaining balance. They are related ideas, but not interchangeable formulas.

Worked Examples

Example 1: $1,000 at 6% for 2 years. Convert 6% to 0.06. Then 1000 * 0.06 * 2 = 120. Interest is $120, total repayment is $1,120.

Example 2: $10,000 at 4% for 3 years. 10000 * 0.04 * 3 = 1200. Interest is $1,200 and total repayment is $11,200.

Example 3: 18 months at 8% on $5,000. Convert 18 months to 1.5 years. Then 5000 * 0.08 * 1.5 = 600. Interest is $600.

Example 4: Zero-interest monthly payment estimate. If a $12,000 loan had 0% interest over 24 months, the monthly payment would simply be 12000 / 24 = 500. This helps illustrate how interest changes the payment structure.

Example 5: Why monthly payment math differs. A fixed monthly payment on a real installment loan depends on rate, number of months, and the balance schedule. That is not the same structure as I = P * r * t.

Example 6: Rate comparison intuition. If two short-term borrowing offers use the same time period but one rate is clearly higher, simple-interest math helps you see the difference quickly before you look at more detailed contract terms.

Common Mistakes

The most common simple-interest mistake is forgetting to convert a percent into decimal form. Another is mixing time units, such as using months with an annual rate without conversion. Students also confuse interest alone with total repayment and may report one when the question asks for the other.

A more advanced mistake is using the simple-interest formula on a problem that clearly describes a fixed monthly payment loan. Once periodic payments and a declining balance are involved, the model has changed.

Readers also sometimes think a simple-interest result is a legal or contractual quote. It is not. It is an educational or planning estimate unless it matches the exact loan terms in the actual document.

FAQ

Does simple interest describe most real loans?

No. Many consumer loans use amortized monthly payments or other compounding structures. Simple interest is still valuable as a teaching model and rough estimate.

Why does time conversion matter so much?

Because the rate and time must match. Annual rate with months is inconsistent unless you convert one of them.

Can a simple-interest estimate still be useful?

Yes. It helps build intuition and offers a baseline for comparison, even when the final contract uses more detailed calculations.

Difference from Nearby Tools

Use the Loan Calculator when you want both a simple-interest estimate and a rough monthly-payment calculation on one page. Use the Percent tool if you need help converting rates before inserting them into formulas. Use the Scientific Calculator for longer custom finance expressions.

Learning Advice

Before solving, write down what each letter in the formula represents and check the units. If rate is yearly, time should also be in years. That unit check catches a large share of finance homework mistakes before any arithmetic begins.

It also helps to ask one modeling question before calculating: "Is this really simple interest, or is it a payment schedule problem?" That question matters as much as the arithmetic itself.

The larger lesson is that finance formulas should be chosen by structure, not by familiarity. Simple interest is powerful when the model fits. It becomes misleading when the model changes and the user does not notice.

Applied learning context

How this topic appears in real coursework

In real classes, this topic usually appears inside mixed assignments instead of in isolation. Students may need to combine definitions, formulas, and interpretation in a single response, which is why practicing only one template answer is often not enough. A stronger routine is to check what the question is really asking, identify the required variables, then map the setup to the correct method before calculating.

Common reasoning traps and how to prevent them

The most frequent mistakes happen before arithmetic starts: reading symbols too quickly, mixing units, applying the wrong formula, or skipping assumptions. To avoid this, write a short pre-check line for each problem: identify known values, unknown values, constraints, and expected answer size. This one-minute habit prevents many avoidable errors and improves final answer quality more than repeated button pressing.

How to self-verify before submitting answers

After solving, verify by estimation and by method. Estimation checks whether the result is in a plausible range. Method checks whether each step still matches the original question intent. If either check fails, revise the setup first instead of retyping numbers. This approach builds transferable problem-solving skill, not just short-term answer accuracy.